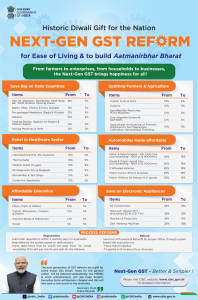

Reforms under GST 2.0

The 56th GST Council announced GST 2.0, introducing next-generation reforms to make the tax regime more citizen-centric, support sectors like agriculture, healthcare, and manufacturing, and enhance ease of doing business.

Changes to GST rates on services will come into effect from 22nd September 2025.

Key Tax Reforms under GST 2.0

1. Simplified GST Structure:

-

Existing four GST slabs (5%, 12%, 18%, 28%) replaced with:

-

5% (Merit rate) for essential items

-

18% (

-

Standard rate) for other goods and services

-

40% (Demerit rate) for luxury, sin, and demerit goods like tobacco and pan masala

-

2. Tax Relief for Essential Goods:

-

Full GST exemption on individual life and health insurance policies

-

Essential items like UHT milk, paneer, and Indian breads now carry nil GST

3. Consumer Goods:

-

GST on small cars, TVs, air conditioners, cement, and auto parts reduced from 28% to 18%

-

GST on renewable energy devices reduced from 12% to 5%

-

The

-

se measures aim to stimulate manufacturing, encourage green energy adoption, and boost domestic demand

4. Medical and Health Devices:

-

GST on 33 lifesaving drugs reduced from 12% to nil

-

GST on three critical drugs for cancer and rare diseases reduced from 5% to nil, improving healthcare access

5. Support for Agriculture and Rural Sectors:

-

Machinery like tractors, harvesters, and composters: GST reduced from 12% to 5%

-

Fertilizer inputs like sulphuric acid, nitric acid, and ammonia: GST reduced from 18% to 5%

-

Labour-in

-

tensive goods such as handicrafts, marble, and leather items: GST reduced from 12% to 5%

6. Trade Facilitation and Dispute Resolution:

-

Goods and Services Tax Appellate Tribunal (GSTAT) to be operational by December 2025

-

Reforms in refunds and registration processes will improve dispute resolution, reduce litigation, and provide predictability for businesses, especially MSMEs

What is GST?

About:

-

Introduced through the 101st Constitutional Amendment Act, 2017, GST is a comprehensive indirect tax levied on the supply of goods and services in India

-

It is a value-added tax (VAT) that replaced multiple indirect taxes previously levied by the Centre and States

Key Features:

-

Dual GST Structure: Central GST (CGST) + State GST (SGST); Integrated GST (IGST) for inter-state transactions

-

GST Council: Primary policymaking body under Article 279A; chaired by the Union Finance Minister with state representatives as members

-

Goods and Services Tax Network (GSTN): Facilitates filing returns, payments, and compliance

-

Threshold Exemption: Small businesses below a certain turnover limit are exempt, reducing compliance burden

Benefits of GST

-

Destination-Based Tax: Levied where goods/services are consumed, improving cash flow

-

Ease of Doing B

-

usiness: Technology-driven, minimal human interface, simplified compliance, refunds, and registration

-

Boost to Make in India: Makes domestic goods competitive nationally and internationally

-

Exports: Supplies to SEZs are zero-rated with quick refunds, promoting trade and improving the balance of payments

-

Revenue & Compliance: Expands the tax base, increases government revenue, enhances transparency, and contributes 1.5–2% to GDP

Achievement of GST

-

In 2024–25, GST recorded its highest-ever gross collection of ₹22.08 lakh crore, a 9.4% year-on-year growth

-

Average monthly collection: ₹1.84 lakh crore