The Pecking Order theory and its relevance in Contemporary finance

The Pecking Order theory- The concept

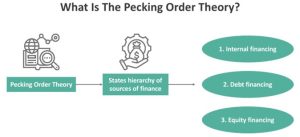

In contemporary finance, the pecking order theory explains how firms prefer a hierarchy of financing sources, starting with internal funds (like retained earnings), then debt, and finally equity as a last resort. This preference is rooted in information asymmetry, where managers possess more company information than external investors, making equity issuance riskier and more costly. While the theory remains a relevant framework for understanding financing choices, its application is being adapted for the digital age due to innovations like big data and AI that can reduce information asymmetry.

The pecking order theory was first suggested by Gordon Donaldson in 1961 and later modified by Stewart C. Myers and Nicolas Majluf in 1984 and is based on the idea that companies face information asymmetry — insiders (managers) know more about the company’s value and risks than outside investors. Because of this, external financing (especially equity) is often viewed skeptically by the market, potentially leading to undervaluation and signaling problems.

Key Components of the Pecking Order

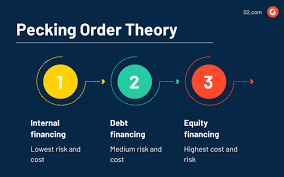

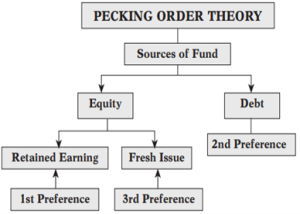

- Internal Financing: Firms first use their own retained earnings and accumulated profits to fund projects.

- Debt Financing: If internal funds are insufficient, firms then prefer to issue debt over equity. Debt is less costly than equity because debt holders have a higher claim on assets than stockholders.

- Equity Financing: New equity is considered the most expensive and is used only as a last resort when other financing options are exhausted.

Reasons for the Pecking Order

- Information Asymmetry (Adverse Selection):This is the core driver of the theory, as proposed by Myers and Majluf. Managers are more informed about a company’s prospects and are more likely to issue equity when their shares are overvalued (the “lemons problem“). Rational investors, aware of this, will buy new equity issues at a discount, which increases the cost of equity for the firm.

- Cost Minimization: Each financing option carries different costs and risks. Using internal funds has no external cost. Debt carries a risk of default, but equity issuance is often more expensive due to the information issues.

Assumptions of POT

- Managers know more about firm value than investors (information asymmetry).

- Firms avoid external financing if internal resources are sufficient.

- Equity issuance often signals that the firm may be overvalued → causing stock prices to drop.

Contemporary Relevance and Evolution

- Digital Age Adaptation: The rise of digital innovations like big data, blockchain, and artificial intelligence (AI) in the digital economy is affecting conventional financing behaviors. These technologies can help to reduce information asymmetry and increase market efficiency, potentially influencing a firm’s financing decisions.

- Mixed Evidence: Empirical studies have provided mixed evidence on the pecking order theory in various economies. While it offers a valuable qualitative framework, determining its precise quantitative impact on a firm’s financing mix can be challenging.

- Empirical Evidence: Research on the POT yields mixed results. Some studies find support for the theory, especially for large firms and in certain economic contexts, while others do not. For example, a study on firms listed on Borsa Istanbul from 2000-2018 found that manufacturing firms generally followed the pecking order, preferring internal funds and then debt as investment levels increased. However, another study on Indonesian firms found that they tend to favor a target capital structure based on the trade-off theory rather than the pecking order.

- Company Size and Type:The POT seems more applicable to larger firms with established financial structures and access to various funding sources. Small and medium-sized enterprises (SMEs) and high-growth companies may deviate from this order due to limited access to debt or the need for equity to fund rapid expansion or address financial difficulties.

- Economic Conditions: Economic factors, such as inflation rates, interest rates, and the development of debt and equity markets, can influence a firm’s financing decisions and affect how closely they adhere to the pecking order.

- Strategic Considerations: Companies may choose to prioritize specific financing options based on strategic goals, such as preserving cash, reducing leverage, or preparing for acquisitions, even if internal funds are available or debt is easily accessible.

Practical application

Despite these limitations, the POT continues to be a relevant concept in financial planning and decision-making for companies.

- Evaluating Financing Options: Finance teams can use the POT to evaluate different financing scenarios based on factors like cost, risk, and market perception.

- Capital Structure Decisions: The theory helps businesses determine the optimal way to raise funds for financing corporate strategies and minimize the cost of capital.

- Investor Communication: When a company needs to issue equity, understanding the POT can help them effectively communicate their financing strategy to investors and mitigate potential negative market reactions.

Relevance in Contemporary Finance (2020s and beyond)

Despite the rise of modern capital markets and evolving financial instruments, Pecking Order Theory still holds value, though with modifications and caveats.

- Behavioral Finance Influence

- In today’s environment, investor sentiment and behavioral biases can amplify information asymmetry.

- Managers may time markets for equity issuance, exploiting temporary overvaluation — which can conflict with the theory’s idea that equity is always a last resort.

- Startups & Tech Firms

- Many high-growth firms rely heavily on equity despite having internal funds or debt capacity. This contradicts the theory.

- However, the theory still explains some behavior: founders avoid external funding early to retain control, then shift to venture capital or IPOs when scaling is required.

- Post-GFC and COVID Financing

- During crises (like 2008 or 2020), companies leaned more on debt (especially government-backed) than equity, aligning with the pecking order.

- However, zero interest rate policies (ZIRP) and QE made debt extremely cheap, which distorts the traditional cost hierarchy.

- Access to Capital Markets

- Larger firms with good credit ratings often go straight to bond markets, while smaller firms may rely more on internal funds or bank debt, partially aligning with the theory.

- The theory is more observable in SMEs than in large, listed firms with sophisticated capital structures.

- Hybrid Instruments

- Contemporary finance offers hybrids like convertible bonds, preferred equity, etc., which blur the line between debt and equity.

- These instruments may be used to manage signaling effects and reduce financing costs, refining the basic theory.

Criticisms and limitations

Despite its merits, the Pecking Order Theory has several limitations in explaining contemporary financial behavior. Primary criticisms include:

- Inconsistent with empirical evidence: Some studies have found that while companies favor internal funding, the evidence does not consistently support a strict pecking order between debt and equity. For example, some highly profitable firms may take on debt for tax benefits or to maintain financial discipline.

- Ignoring the optimal capital structure: Unlike the Trade-Off Theory, which suggests firms aim for an optimal debt-to-equity ratio, the POT does not account for a target capital structure. In reality, firms often manage their debt ratios within a specific range.

- Outdated for modern funding methods: The theory struggles to account for newer financial instruments and funding sources, such as venture capital and private equity, which operate differently from traditional bank loans and public equity issuance.

- Failing for large firms: For large, stable, and transparent public firms, information asymmetry is less of a concern. These companies may have sophisticated capital structures and strategic financing goals that don’t conform to the strict pecking order.

- Lack of quantitative measurement:The theory describes a qualitative hierarchy but does not offer a quantitative method for determining the mix of financing or the exact impact of information costs.

In summary, the pecking order theory continues to be a powerful framework in finance, but its application is evolving to account for new technologies and economic shifts that can alter the information landscape and, consequently, a firm’s capital structure decisions.

*********